Runs on financial institutions are one of the salient markers of financial crises. But the role of runs in crises is a topic of longstanding debate. Runs can be seen as the key turning point, whereby even small shocks can generate severe crises with widespread bank failures. Another view is that runs are mainly a symptom of deeper rot in the financial system, exacerbating crises rather than being their primary cause. Understanding this debate has first order implications for how to think about financial crises and the appropriate policy responses. In this post, we use a new database of more than 3,000 bank runs (introduced in our companion post) to show that poor fundamentals are central to explaining both when runs occur and when they have severe economic effects. We argue that this evidence tempers the view that small shocks can have outsized real effects through self-fulfilling run dynamics.

The Historical Bank Run Database

A key challenge for understanding the causes and consequences of bank runs is the absence of systematic microdata on the occurrence of bank runs. As we detailed in our previous post, we overcome this gap by studying the near-universe of runs in the U.S. banking system from 1863 to 1934 as recorded in contemporary newspapers. We combine this new data on bank runs with data on bank balance sheets, macroeconomic conditions, and local business failures and manufacturing activity.

The historical U.S. banking system provides an appealing environment to study runs. Our sample covers the numerous panics of the National Banking Era and the Great Depression. This contrasts with the contemporary banking system, where runs are much less common due to a variety of government interventions that affect depositor behavior, such as deposit insurance and lending of last resort.

Finding #1: Runs Are Considerably More Likely in Weak Banks but Can Also Occur in Strong Banks.

We first document that runs are substantially more likely in banks with weak observable fundamentals. To establish this finding, we construct a simple summary measure of bank health (“fundamentals”) based on variables measuring a bank’s capitalization, profitability, and ability to finance itself with cheap deposits relative to expensive noncore funding. Existing research shows that these metrics capture bank health and failure risk (Correia, Luck and Verner, 2025).

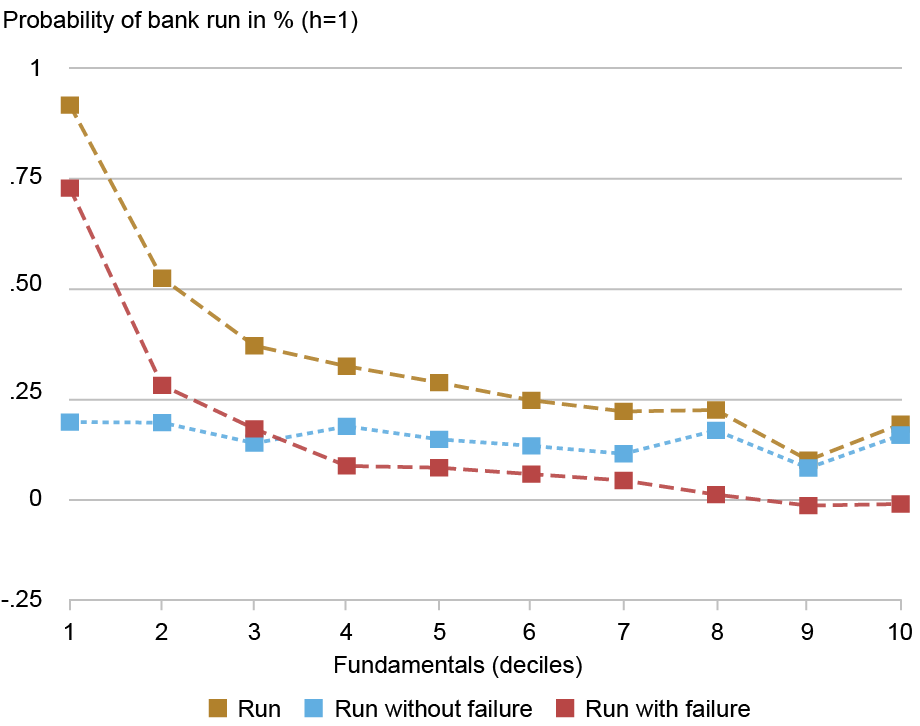

The chart below provides a visualization of the relationship between bank fundamentals and the likelihood of a run, a run with failure, and a run without failure across deciles of our proxy for fundamentals. The gold line shows that runs are more likely in banks with weak fundamentals. A bank in the lowest decile of fundamentals has a nearly 100 basis point probability of being exposed to a run in a given year, whereas the probability is only about 25 basis points for banks with strong observable fundamentals. Thus, runs on strong banks are less common, but they can occur. Moreover, the absolute probability of a run for weak banks is relatively low.

Probability of Bank Runs by Bank Fundamentals

Notes: This chart plots the probability of a bank run, a bank run that does not result in failure, and a bank run that does not result in failure across deciles of a proxy of bank-specific fundamentals (see text for definition).

Finding #2: Runs Typically Only Result in Failure for Banks with Weak Fundamentals.

How common is it for runs to result in bank failure? We find that a bank has a 38 percent probability of failing if it is subject to a run. This is a high conditional probability of failure, given that the annual unconditional probability of bank failure is 0.85 percent. At the same time, it also implies that a run is not a death sentence. There are more runs without bank failure than runs with failure, highlighting a key novel insight from our approach.

We further establish that whether a run results in failure depends crucially on a bank’s financial health. The chart above decomposes runs into those where the bank fails and those where it survives. It shows that runs are significantly more likely to result in failure for banks with weak fundamentals. In our paper, we estimate that conditional on a run, a bank with very weak fundamentals—defined as being in the lowest decile of our preferred metric that summarizes a bank’s financial health—has a 63 percent probability of failing. In contrast, the strongest banks, measured as being in the top decile of the same metric, essentially never fail when subject to a run. Thus, weak bank fundamentals are necessary for a run to be associated with bank failure.

How Do Strong Banks Survive Runs?

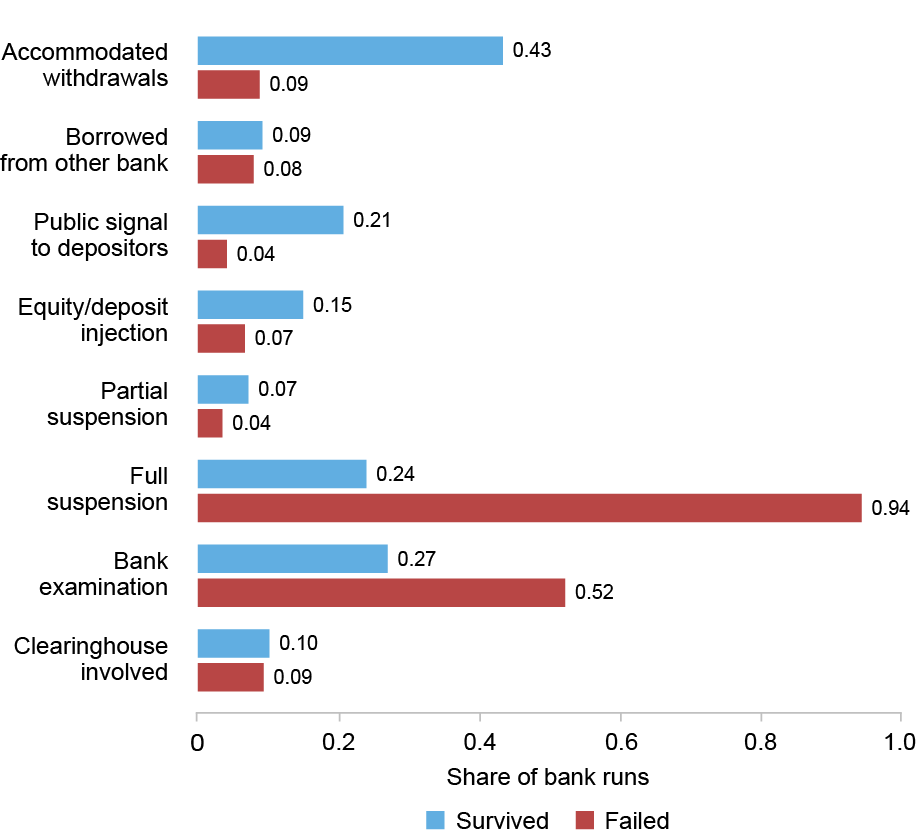

Banks with strong fundamentals typically do not fail when subject to a run. This raises the question: How do strong banks survive runs? What measures do banks take to fend off runs? To better understand how banks with sound fundamentals are able to survive runs, we analyze how newspapers describe banks’ responses to runs. We identify seven common responses discussed in newspapers. The chart below shows the share of run episodes mentioning each of these responses, distinguishing between runs that result in failure and runs where the bank survives.

The first step banks take in response to runs is to accommodate withdrawals and attempt to signal strength to depositors, such as delivering a “truckload of cash” to the bank. To obtain additional cash, bank owners would sometimes inject additional equity into the bank or borrow from other banks. To conserve liquidity and cool the run, banks would often partially suspend convertibility, invoking 30-/60-day notice rules for savings deposits. In extreme runs, banks fully suspend convertibility. Suspension was often coupled with examinations by state supervisors, federal examiners, or the local clearinghouse to evaluate if the bank was solvent. When these banks are deemed to be insolvent, they are closed. Finally, in about 10 percent of runs, newspapers explicitly mention the involvement of clearinghouses, either through the provision of a loan, examination, or other measure. These measures enabled solvent banks to survive runs, severing the link between illiquidity and insolvency.

Bank Responses to Runs Discussed in Newspapers

Notes: This chart plots the share of episodes involving a bank run in which the newspapers mention one of the listed actions. The shares are reported separately for runs without and with failures.

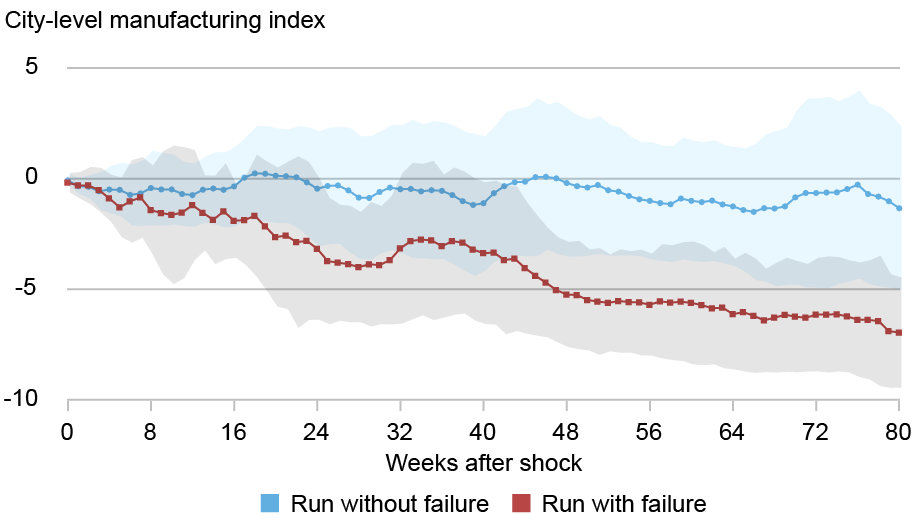

Finding #3: Runs on Weak Banks Lead to Substantially Larger Local Declines in Deposits, Lending, and Manufacturing Activity than Runs on Strong Banks.

To study the real economic effects of runs at the local city level, we use data on historical local economic activity constructed from issues of Bradstreet’s from 1917 to 1935. Bradstreet’s was a business journal that provided, among other things, summaries of economic conditions at a weekly frequency in major cities for various sectors, including manufacturing, retail trade, and wholesale trade.

The chart below reveals that runs in which the bank fails predict substantially worse declines in local economic activity than runs without failure. Runs without failure do not result in significantly lower manufacturing activity within the next eighteen months. In contrast, runs with failure predict a decline in manufacturing activity of over 5 percent. This evidence argues against the view that runs that originate as pure liquidity events can generate severe disruptions in local credit markets and real activity. Runs on strong banks carry limited adverse effects beyond the affected banks. Instead, the evidence indicates that poor fundamentals are necessary for runs to generate severe local financial disruptions.

The Effect of Bank Runs on Local Manufacturing Activity

Wrapping Up

Our findings lend little support to the view that small shocks by themselves can result in widespread banking panics that cause major economic downturns. In contrast, our findings suggest that poor bank fundamentals are necessary for bank runs to translate into failure and for bank distress to generate severe economic distress. Although runs can occur in both weak and strong banks, poor fundamentals are necessary for runs to result in bank failures. Runs should thus be seen as a trigger for bank failures and crises, but insolvent banks are necessary for this trigger to devastate the banking system and the economy.

Sergio Correia is a senior economist at the Federal Reserve Bank of Richmond.

Stephan Luck is a financial research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Emil Verner is the Lemelson Professor of Management and Financial Economics and a professor of finance at MIT Sloan School of Management.

How to cite this post:

Sergio Correia, Stephan Luck, and Emil Verner, “What Do Over 3,000 Bank Runs Teach Us About Banking Crises?,” Federal Reserve Bank of New York Liberty Street Economics, July 7, 2026, https://doi.org/10.59576/lse.20260707b

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).