In the third quarter of 2025, America’s largest tech firms for the first time spent more on capital investment than they earned from operations. The implication is that AI, a technology with the potential to make the economy more productive, is, for now, absorbing resources faster than it is generating returns. This post discusses how the tension between AI’s long-run promise and its short-run costs affects the outlooks for inflation, real activity, and financial stability.

Three Channels, One Framework

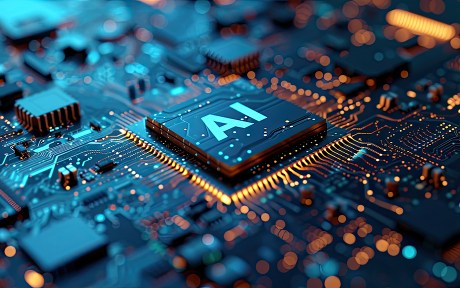

Drawing on my research, I describe three interrelated channels—inflation dynamics, structural transition, and financial stability—through which AI bears on the economy (see figure below).

Three Channels Through Which Diffusion of AI Can Affect the Economy

Inflation Dynamics

In the short run, the diffusion of AI can reshape how interest rates influence inflation and real activity. A widely held view is that AI, by raising productivity, will be a powerful disinflationary force. This view may ultimately prove correct, but it skips a crucial step. What matters for inflation is not whether AI raises productivity, but whether it raises productivity faster than it increases the costs of adopting it.

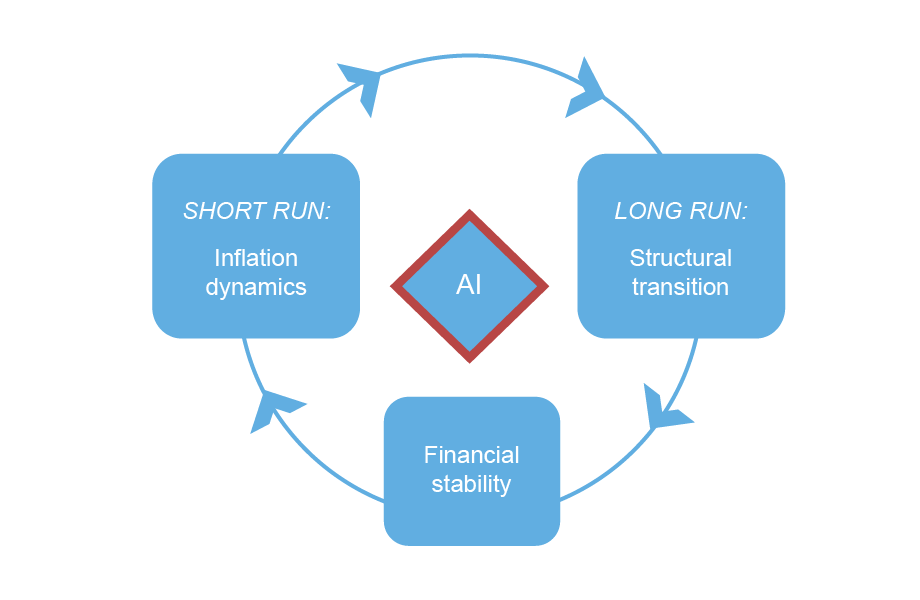

During the transition, firms divert substantial resources toward reorganization, data infrastructure, and integration, which can temporarily raise production costs even as the technological frontier expands. This is the so-called “productivity J-curve,” depicted in the figure below.

Measured Productivity Can Fall During the Adoption Phase

The effects on prices, on the other hand, are already visible in input markets. In 2025, the major AI firms (Google, OpenAI, Anthropic, Meta, Amazon, Oracle) committed roughly $300 billion to capital investment across semiconductor supply chains, power grids, and specialized labor. Aggressive investment spending continued into the first quarter of 2026 and is projected to rise further, adding to cost pressures across the economy.

Recent data suggest that AI-driven demand has been pushing prices up over the past two years, and those costs are now passing through to prices of consumer electronics. For example, the prices for memory chips are up substantially. A recent report indicates that energy consumption and prices are also being affected.

Structural Transition over the Long Run

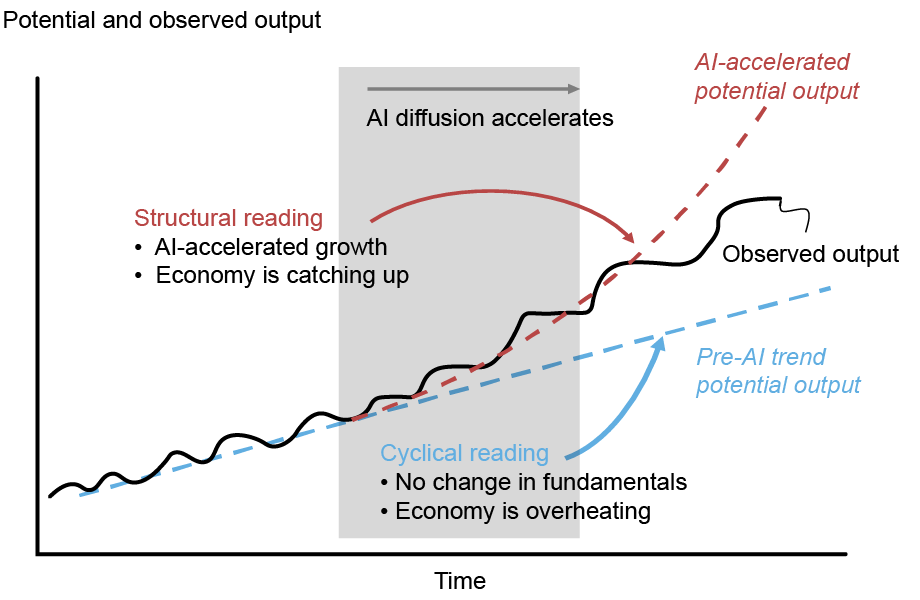

AI may shift the economy’s fundamentals: the level of potential output and the natural rate of interest. The critical question is whether AI generates a one-time level shift in productive capacity or a sustained acceleration in growth (see figure below). A level shift temporarily raises the natural interest rate during the transition before growth reverts to baseline, while a growth acceleration raises it permanently.

Faster AI Adoption Can Signal Either That the Economy Is Overheating or That It’s Catching Up to Its AI-Lifted Potential

To date, estimates of the productivity impact span both scenarios, from modest gains of a few percentage points of GDP over a decade to considerably larger effects if AI augments the innovation process itself. The range is wide and the uncertainty is compounded by countervailing forces, including a possible increase in market concentration and shifts in household saving and spending.

Concentration matters because AI adoption tends to be skewed toward large firms: if rents accrue to a handful of incumbents, the investment boom that lifts the neutral rate may prove narrower than aggregate figures suggest, and winner-take-all dynamics may also slow the diversity of research that sustains long-run growth. On the household side, the fall in consumption among workers whose tasks AI displaces may be only partially offset by the gains of those it complements. If the latter tend to save a higher share of their earnings, aggregate consumption may be weaker than productivity figures alone would suggest.

Financial Stability

AI is rewiring the financial system. Until recently, the major AI companies funded capital investment almost entirely from retained earnings, insulating the AI buildout from credit-market conditions.

That changed in late 2025: capital expenditures began to exceed operating cash flows, and the firms raised over $100 billion of new debt. Beneath those headline bond issues lies a more intricate layer—off-balance-sheet project finance vehicles funding data center construction, securitizations backed by lease cash flows, and hundreds of billions in forward lease commitments that will not appear on balance sheets for years. Much of this debt is predicated on AI productivity returns that have not yet materialized. If expectations shift, the correction could travel quickly and widely: the same institutions—insurers, asset managers, pension funds—hold overlapping exposures across corporate bonds, securitizations, and private placements, so a broad repricing would hit them from multiple directions at once.

Putting AI in Perspective

1. AI’s Centrifugal Bind

The three channels described above do not operate independently, and their interaction creates a challenge in tracking the economy. Consider the following scenario. AI adoption initially raises costs without raising productivity (the J-curve), while firms, consumers, and markets already expect solid gains ahead. Inflationary pressure builds from the supply side: firms’ production costs rise as input markets tighten due to, for example, higher prices for memory chips and energy. Demand-side pressure builds too: expectations of future productivity sustain elevated asset valuations and support spending today, before the productivity gains arrive. And the financial system is exposed: a wave of capital expenditures financed with debt is predicated on returns that have not yet materialized.

The result is what physicists would call a centrifugal bind: forces pulling outward in opposite directions. Higher inflation could puncture asset valuations built on real but distant productivity gains, triggering financial stress precisely when the supply-side payoff has yet to arrive. Efforts to protect financial stability enable the cost and demand pressures to compound. Both forces are real and trace back to the same underlying gap between what AI is expected eventually to deliver and what it is actually delivering now.

2. Rethinking “Long and Variable Lags”

Milton Friedman observed that policy works with “long and variable lags”—that when a central bank adjusts rates, the effects on inflation and activity take months or even years to materialize, and the timing shifts unpredictably across episodes. His point was not just that the real effects of policy are slow, but that they are slow in ways that cannot be reliably anticipated. AI unsettles this tenet in two ways.

First, AI may reshape which lags are long and which are short. Some lags may compress: faster information flows, algorithmic pricing, and more elastic expectations speed up transmission. Other lags may lengthen: reorganization costs and factor market frictions mean supply-side adjustments can take years and move in the wrong direction first. The result is not a uniform shortening but a reshaping of timing and direction, unlike anything historical models were built to handle.

Second, even if the lags themselves don’t change, the rapid diffusion of AI complicates the distinction between cyclical fluctuations and structural shifts. During a major technological transition, it becomes genuinely hard to tell whether output is rising because demand is overheating or because the economy’s speed limit is expanding. The trouble is that the data look identical under both interpretations, often for years.

3. A Cautionary Tale from the Dot-Com Era

The IT revolution of the 1900s offers a cautionary precedent. In the 1990s, Fed Chairman Alan Greenspan resisted calls to tighten prematurely, betting that IT was expanding the economy’s productive capacity. He was right. But the dot-com crash that followed showed that even when the supply-side narrative is broadly correct, expectations can generate asset-price dynamics that create independent financial stability risks. Getting the trend right did not protect against the bubble.

Today’s AI cycle features some of the same tensions as that episode—uncertain productivity effects, difficulty distinguishing supply from demand, and expectations-driven asset dynamics. But it is unfolding within a layered and leveraged financial system. As a result, the path toward an AI-driven high-productivity economy might prove to be a bumpy one.

Simone Lenzu is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Simone Lenzu, “AI’s Macroeconomic Challenges and Promises,” Federal Reserve Bank of New York Liberty Street Economics, May 20, 2026, https://doi.org/10.59576/lse.20260520

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).